How hateful rhetoric connects to real-world violence |

- For LGBTQ+ students, this year’s Pride Month comes at a perilous time

- But CAN the United States defend Taiwan?

- What if the Federal Reserve books losses because of its quantitative easing?

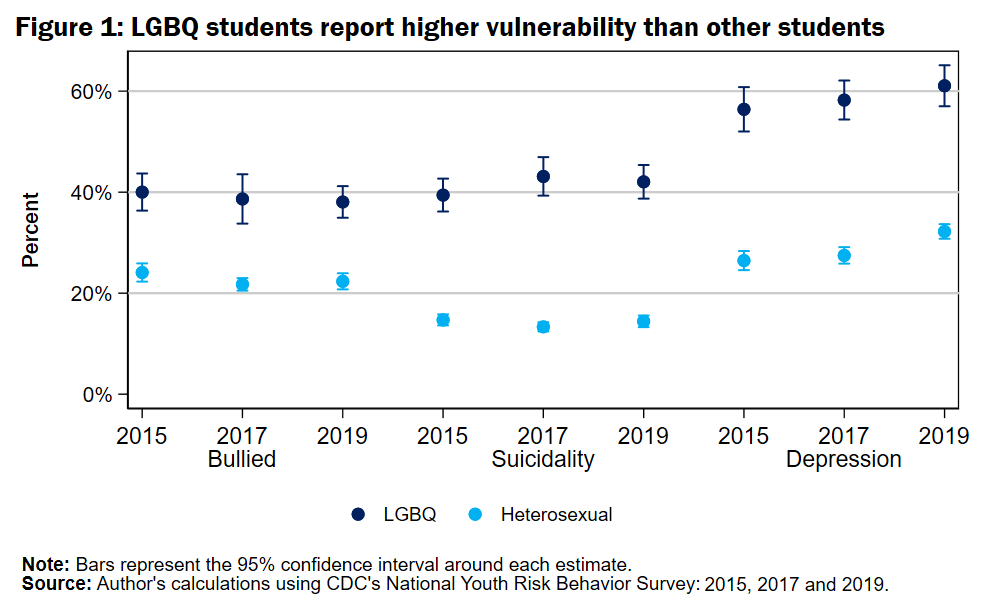

| For LGBTQ+ students, this year’s Pride Month comes at a perilous time Posted: 01 Jun 2022 11:23 AM PDT By Joel Mittleman The year 2015 marked a historic milestone in the struggle for LGBTQ+ rights: the Supreme Court's recognition of marriage equality. The court's ruling both reflected and promoted an incredible sea change in American life. In the two decades prior to the decision, public opinion on LGBTQ+ rights improved more rapidly than any other attitude in the history of American opinion polling. Growing up amid these changes, today's LGBTQ+ youth are the beneficiaries of tremendous social progress. The markers of this progress are easy to find. Lesbian, gay, and bisexual youth are coming out earlier than ever before. Whereas older generations report not coming out until their mid-20s, those born in the 1990s report coming out while still in high school. Not only are today's LGBTQ+ youth coming out at younger ages, they're also coming out in greater numbers. Driven largely by a rapid increase in bisexuality among younger cohorts of women, the number of young people identifying as LGBTQ+ continues to rise. The increasing visibility of LGBTQ+ youth is actively reshaping America's schools. Beginning in 2015, the Department of Education's School Survey on Crime and Safety began asking principals whether their school had a recognized club to "promote acceptance of sexual orientation and gender identity (e.g., Gay-Straight Alliance)." In 2015, 12% of middle school principals and 50% of high school principals reported having such clubs. By 2017, principals reported gay-straight alliances in 23% of middle schools and 59% of high schools, including 76% of suburban high schools, 72% of urban high schools and 39% of rural high schools. In 23 states, these school-level clubs are supported by state-level policies explicitly prohibiting bullying on the basis of sexual orientation and gender identity. In so many ways, it would seem that there's never been a better time to grow up LGBTQ+ in America. And yet, in the same year that the Supreme Court ruled in Obergefell, America also reached another milestone in its recognition of LGBTQ+ populations. Although less momentous, it too was the result of generations of research and advocacy. For the first time ever, the CDC included a question about sexual identity in its national Youth Risk Behavior Survey (YRBS). This survey provided the first population-based, nationally representative portrait of sexual minority high school students since the Add Health study two decades prior. The results were sobering. Among students who identified as lesbian, gay, bisexual, or "not sure" (LGBQ), about 40% reported being bullied, 39% reported having "seriously considered" suicide, and a full 56% reported clinically significant signs of depression. Although some of the CDC's estimates were later shown to be inflated by "mischievous responders," these bullying and mental health disparities remained remarkably stable across analyses. Since 2015, the story told by America's LGBQ high school students has not improved. (Because these data do not assess gender identity or sexual identities beyond L/G/B/Q, I refer here only to LGBQ students). In Figure 1, I present estimates from the 2015, 2017, and 2019 National YRBS. For LGBQ respondents, the results show no change in bullying, no change in suicidal ideation, and a slight upward trend in depression. On every measure, LGBQ students report substantially worse outcomes than their straight peers: LGBQ students are about 70% more likely to report bullying, twice as likely to report suicidal ideation, and three times more likely to report depression. Population-representative data on transgender students are more limited. However, the data that are available provide a picture of an especially vulnerable population, reporting outcomes similar to or worse than those reported by LGBQ students. Early indications suggest that the experiences of LGBTQ+ teens only worsened during the COVID-19 pandemic.

Compared to social and legal contexts faced by generations before them, things have surely gotten better for today's LGBTQ+ youth. But the realities reported in the YRBS provide a painful perspective on how far America still needs to go to achieve equality for its LGBTQ+ populations. That perspective is all the more urgent in the current moment. Following the recent period of historic progress, a far-reaching and well-orchestrated backlash against LGBTQ+ rights is now in full swing. After seeing just a handful of anti-LGBTQ+ bills introduced in state legislatures in 2018 and 2019, the past three years have witnessed a record-breaking number of anti-LGBTQ+ measures proposed and passed across the country. In just the first three months of 2022, lawmakers proposed 238 bills restricting the rights of LGBTQ+ Americans. Many of these bills specifically target LGBTQ+ students' experiences within schools. These legislative initiatives also appear to have emboldened a wave of LGBTQ+ book bans, efforts to dismantle gay-straight alliances, and the forced removal of LGBTQ+-affirming materials from school spaces. And so, this year's LGBTQ+ Pride Month comes at a perilous time. A growing body of population-representative data reveals just how far away the promise of equality remains for today's LGBTQ+ youth. At the same time, rising waves of anti-LGBTQ+ legislation offer a stark reminder that continued progress toward equality is by no means assured. To push back against this tide, there is much that can be done. Citizens can support policies protecting LGBTQ+ students and teachers. School leaders can promote gay-straight alliances, which serve as a critical protective factor at times when LGBTQ+ bullying is on the rise. And individual teachers can continue to make a tremendous difference, since the presence of even one LGBTQ+ affirming teacher in a school is associated with significantly better academic and emotional outcomes for LGBTQ+ youth. Although Pride Month comes at the end of the school year, this is no time to take a break. When even foundational rights like marriage equality appear newly uncertain, this year's Pride is a time not only to celebrate, but to organize. This posting includes an audio/video/photo media file: Download Now |

| But CAN the United States defend Taiwan? Posted: 01 Jun 2022 11:20 AM PDT By Michael E. O'Hanlon President Joe Biden has yet again stated that if China attacked Taiwan to reunify what Beijing sees as a renegade province with the mainland, the United States would come to Taiwan's military defense. White House staff has again followed up these off-the-cuff presidential comments with a "clarification" that in fact, strategic ambiguity remains American policy. Somewhat oxymoronically, the United States seeks to be crystal clear about being intentionally unclear about what we would do (evocative of British policy just before World War I on whether London would come to Paris's aid, should France be attacked). The goal is to avoid emboldening Taiwan to provoke China even as we try to deter China in the event it does feel provoked. Quite the balancing act. But here's the real rub: Saying we WOULD defend Taiwan militarily does not mean we COULD do so successfully. These doctrinal debates over strategic ambiguity versus strategic clarity seem strangely disconnected from military reality. America's policy of strategic ambiguity was born during the Cold War, when it was a simple fact that the United States enjoyed overwhelming military dominance against China in the waters and airways of the western Pacific. Even though Taiwan was 100 miles from China and thousands of miles from the United States, U.S. dominance in advanced air and naval weaponry meant that we almost surely could have come to Taiwan's defense and prevailed. Given China's dramatic military modernizations of recent times, the situation is now much more complex. Recent analysis that I have done at Brookings indicates that especially for certain types of blockade scenarios by which China might seek to squeeze Taiwan into submission, the United States and its allies might still win a war in which they sought to break the blockade. But we also might lose it. In general terms, a possible naval blockade of Taiwan offers advantages to China. For this scenario, unlike that of an attempted invasion, trends in technology favor rather than hurt China, since it would be the actor threatening large military objects like ships and airfields and ports. To minimize China's own vulnerabilities, People's Liberation Army Navy attack submarines might be the principal assets employed, rather than surface ships or aircraft. Cyberattacks would likely support the physical operation. Beijing might escalate to the use of land-based missiles and aircraft later in a battle, depending on initial results. And all of these operations, and the effectiveness of their counters, would surely fluctuate over time. The opposing sides would seek the best places to operate (given sonar conditions and other considerations) and would vary the intensity of their efforts as a function of their effectiveness, and of the interplay between military operations and broader political dynamics in Beijing, Taipei, Washington, Tokyo, and beyond. My modeling strongly suggests that the outcome of such a conflict over Taiwan is inherently unknowable. That is true, I believe, even if the battle is assumed to remain within reasonably specific boundaries of possible escalation. I cannot prove my conclusion beyond any reasonable doubt with simple models that depend on unclassified and potentially dated input data to generate their results. But it is doubtful that planners on either side with access to more complex models and more current data can do much better. There are simply too many major technical uncertainties — about the performance of command and control systems, undersea warfare, and possibly missile defenses, in addition to questions about resilience and reparability of the in-theater ports and runways upon which U.S. operations would depend — to permit reliable prognostication. The possibility of escalation to wider or even nuclear war of course reinforces these specific uncertainties about a more concrete scenario centered on a blockade. The best that modeling can do to handle these variables is to create reasonable boundaries within which actual scenarios might generate their actual results. So long as those boundaries are difficult to dismiss, and include cases in which both sides win, anyone entering a war confident of knowing the winner in advance has a high analytical threshold to establish. Thus, although it is possible that planners on one side or the other (or both) could develop plausible theories, and concepts, of victory — perhaps akin in some ways to Germany's war plans against France and Britain of 1914 and 1940 — defeat must be considered an equally plausible outcome. This conclusion should be sobering for any leader who might consider risking such a conflict in the years to come. The implications of a responsible approach to modeling and analyzing warfighting scenarios are important not only because they should affect leaders' assessments of the risk of war, but also for purposes of U.S. and partner force planning. Model results might for example suggest certain modifications to or modernizations of key assets to reduce vulnerabilities, especially in command and control, but also in supply and maintenance, in ordnance sustainability, and in the adequacy of anti-submarine warfare assets including planes, ships, and submarines within the U.S. military force structure. But even more, the implications should affect how all parties think about crisis management and any use of force. China should not see such limited-force scenarios as somehow safe or controllable; the United States should not necessarily respond to a Chinese blockade with a prompt counterblockade operation, if it can devise alternative approaches. The United States should respond to any Chinese attack, yes — in that sense, there should not be strategic ambiguity — but rather than promise to respond militarily, we should seek to develop a wider range of response options that include the use of economic, diplomatic, and other tools. This approach has the benefit of being consistent with the Defense Department's concept of "integrated deterrence," and of not promising that we would effectively defend Taiwan when in fact it may be beyond our power to do so. This posting includes an audio/video/photo media file: Download Now |

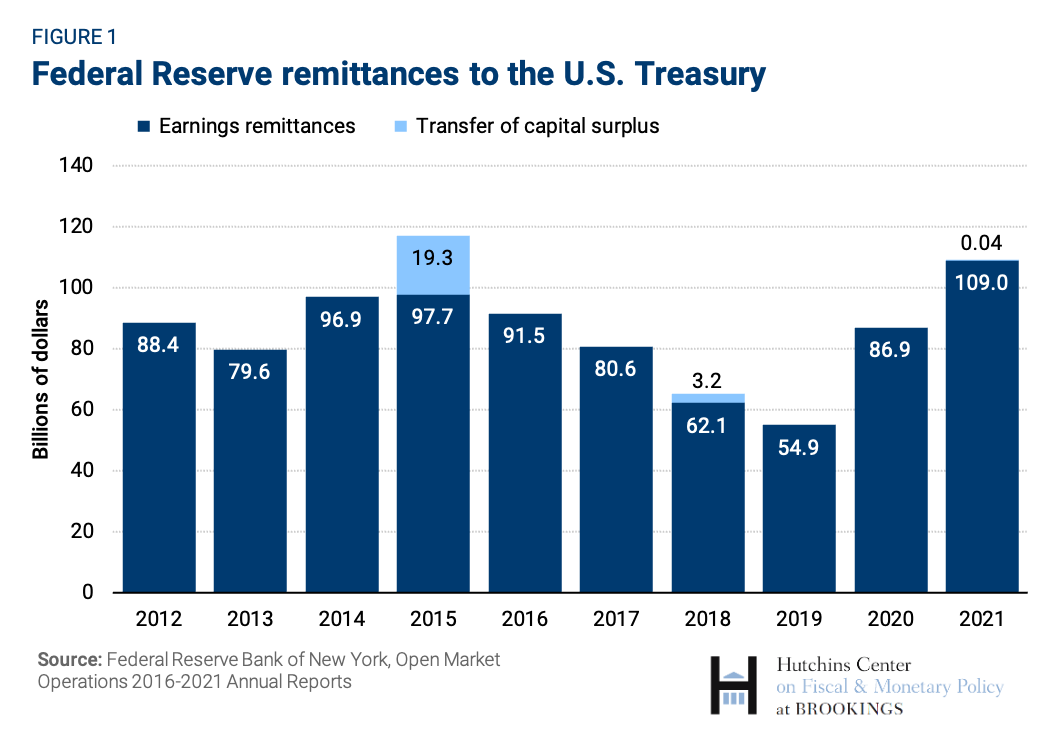

| What if the Federal Reserve books losses because of its quantitative easing? Posted: 01 Jun 2022 09:40 AM PDT By William B. English, Donald Kohn In the course of making monetary policy and issuing currency, the Federal Reserve accumulates a portfolio of Treasury and agency securities, which earn interest. Its liabilities consist primarily of currency outstanding, which of course pays no interest, deposits of the U.S. Treasury, which also pay no interest, and reserve deposits of banks and repo borrowing from money market funds and other lenders, both of which do pay interest. Normally, the interest the Fed earns on its securities greatly exceeds the interest it pays to banks and money funds, and the Fed meets its expenses from the surplus and remits the rest to the Treasury. In response to the COVID pandemic, the Federal Reserve used quantitative easing (QE) – that is, large-scale purchases of Treasury securities and agency mortgage-backed securities – both to support market functioning and to ease financial conditions and strengthen the economic recovery. Its securities portfolio grew from less than $4 trillion to $8.5 trillion between March 2020 and March 2022.[1] Over the same period, currency expanded from $1.8 trillion to $2.3 trillion, and the Treasury's account at the Fed rose from $0.4 trillion to $0.6 trillion. Despite the more modest growth in the Fed's noninterest liabilities, the interest earnings on the Fed's securities holdings increased much more than the interest paid on its liabilities, and the Fed's remittances to the Treasury rose from $55 billion in 2019 to $87 billion in 2020 and $109 billion in 2021.

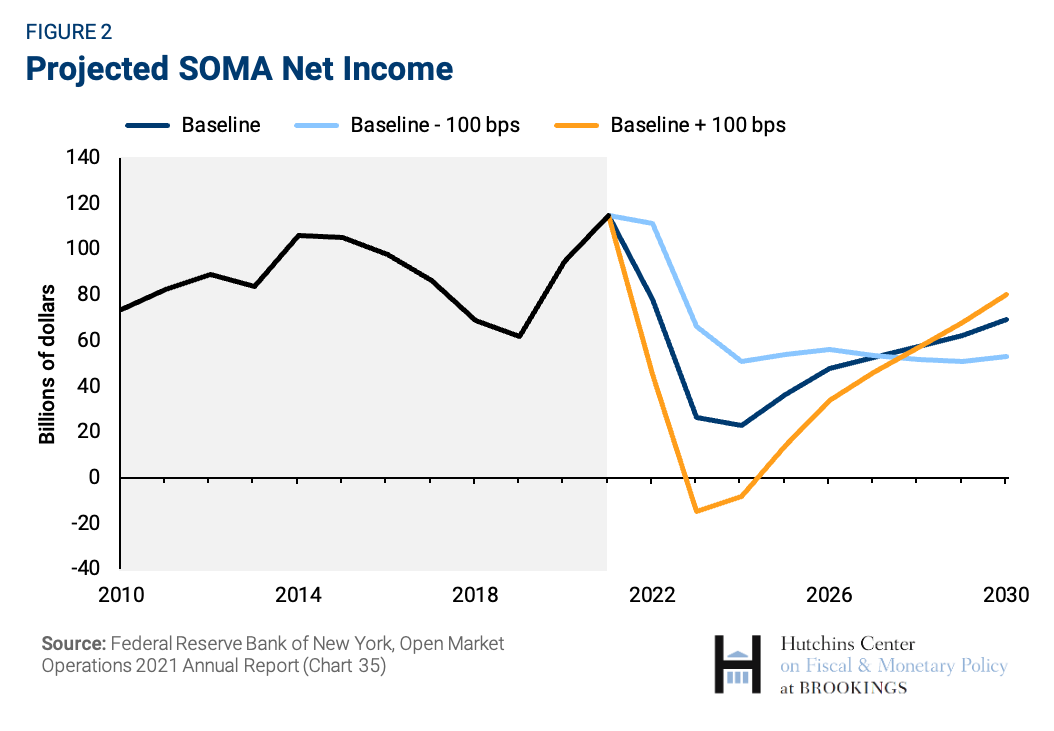

However, with the Fed now raising rates "expeditiously," the Fed's net interest income on its securities holdings will fall as the rate earned on the securities it holds remains relatively fixed while the interest rate it pays on its liabilities rises. The Fed has noted that if interest rates rise sufficiently high, it could end up paying more out in interest than it takes in, resulting in a loss for the Fed.

This post discusses whether such losses have significant implications for monetary policy, and the extent to which the Fed's losses are a cost to the taxpayer and the broader U.S. economy.[2] What would happen if the Fed had a loss?If the Fed booked a loss in a given year, it would have no profits to remit to the Treasury. Under the Fed's accounting rules, it would then accumulate a "deferred asset" equal to its cumulative losses. Once the Fed returned to profitability, it would retain profits to pay down the deferred asset. Only once the deferred asset had been reduced to zero – that is, once the Fed had retained earnings offsetting its earlier losses – would the Fed resume remitting profits to the Treasury. (For details, see Carpenter et al (2015)). Would those losses have any implication for the Fed's ability to make monetary policy?No. Despite any plausible losses, the Fed could continue to operate normally and implement monetary policy. In particular, the Fed could still raise and lower its target range for the federal funds rate and adjust the size of its portfolio to influence financial conditions as appropriate given economic conditions. Should the Fed worry about possible losses in setting monetary policy?The Fed is not a profit maximizing institution. It is not a bank or a hedge fund. It is, rather, a public institution with public objectives. The Fed's monetary policy objectives, as set by Congress, are maximum employment and stable prices. And Congress has given the Fed tools to use to foster those objectives, including the ability to control short-term interest rates and the authority to purchase Treasury and agency securities. While purchases of longer-term securities can, in some circumstances, lead to losses for the Fed, the Fed's mandate is neither to make profits or to avoid losses. The Fed should use its tools to achieve its mandate. Are Fed losses a problem for the Treasury and the taxpayer?Although unexpected increases in interest rates can lead to Fed losses and lower-than-expected remittances to the Treasury, there are a number of reasons why losses for the Fed are not equivalent to losses for the taxpayer or for the country as a whole. First, even if QE leads to Fed losses in some periods, it will likely also boost Fed profits in other periods.[3] Thus, the losses in a given year may simply offset a portion of the profits in other years, leaving the overall effect on Fed income positive. Second, the Fed does QE to put downward pressure on longer-term interest rates. Thus, if the policy is effective, QE will reduce the interest that the Treasury pays on its long-term debt. So even if the Fed has losses over time on its holdings, there may be no net loss for the Treasury and thus for the taxpayer. Third, the easier financial conditions caused by the QE help boost output and employment – indeed, that is the point of conducting QE when the Fed's short-term policy rate is constrained by its lower bound. But higher output and employment increase tax revenues and reduce government expenditures on safety net programs. Thus, the net effect of QE on the budget can be positive even if the Fed has losses for a time. One way to summarize the effects of QE on overall costs to the taxpayer is to look at the cumulative effect of the QE on the ratio of federal debt to GDP over time. In a memorandum to the FOMC, Clouse et al (2013) used the FRB/US model to evaluate these different effects. Their analysis indicates that, even in cases where interest rates rise considerably faster and further than expected and the Fed posts significant losses, the total effect of QE can be to reduce the debt-to-GDP ratio. That is, despite the Fed's losses, the taxpayer can be significantly better off with the QE. And, of course, the effects on Treasury finance are not a full measure of the welfare effects of the QE. Since output and employment will be higher as a result of QE, many workers and their families will be better off, regardless of the effects on the federal budget. In short, when considering the desirability of QE, policymakers need to assess the full set of its effects and should not focus on the Fed's income statement. But couldn't Fed losses lead it to default in some way, causing a financial crisis or high inflation?The Fed can't default because it can always create reserves to pay its bills. Moreover, the banking sector must hold the reserves created by the Fed, so the Fed cannot suffer from a run on its funding. That said, if the Fed had large enough losses for a long enough time, it would have to create such a large amount of interest-bearing liabilities to cover its expenses that it wouldn't be able to implement monetary policy appropriately. (In terms of the Fed's accounting, its losses could outstrip all its future profits.) In that extreme case, the Fed would need to get fiscal support from the Treasury. At times, some foreign central banks have had losses in excess of their capital and nonetheless continued to operate effectively (Chaboud and Leahy, 2013). Happily, the Fed's future profits are likely to be substantial, since more than $2 trillion of its securities holdings are financed by currency, on which the Fed pays no interest. Given the low level of real interest rates in recent years and the likely growth of currency along with the economy, the present discounted value of future Fed profits is very large – in the trillions of dollars – and so it would take truly colossal and highly improbable losses before the Fed might be unable to implement monetary policy effectively. (Hall and Reis (2015) examine this issue.) Even if the Fed can't default, couldn't losses undermine the Fed's independence?Even if Fed losses don't constrain monetary policy or necessarily impose a cost on taxpayers, the Fed's actions often are controversial. Substantial losses could trigger criticism on Capitol Hill, particularly if rising interest rates become a political issue. Even short of losses on the Fed's books, rising interest rates increase the cost of financing the national debt. Eliminating Fed remittances for a few years as a result of losses would make the budget situation even more challenging. However, like monetary policymakers, politicians and the public should take account of the full range of effects of QE and not focus undue attention on Fed income. The Fed can help foster such a balanced assessment by using its communication and outreach to ensure that the public and the Congress understand the benefits of QE and how it can help the Fed achieve its policy objectives, as well as the potential risks. In order to allay any concerns, the Fed should emphasize now that losses will not constrain its ability to continue to implement monetary policy in the pursuit of its maximum employment and price stability objectives. [1] Indeed, Fed remittances to the Treasury have averaged $72 billion per year since the first QE program was introduced in late 2008, nearly three times the $26 billion per year averaged over the previous decade. [2] The Fed values its securities on an amortized cost basis—hence if it does not sell its securities, the net earnings on its portfolio reflect only net interest income. However, the Fed does publish the unrealized capital gains and losses on its holdings on a quarterly basis. Unanticipated economic developments can lead to changes in the expected path of short-term interest rates, which will result in changes in both expected Fed income and the market value of the Fed's securities holdings. However, the value of the Fed's portfolio can also change as a result of expected movements in short-term interest rates that do not have implications for expected Fed income. [3] The Fed's portfolio was as large as it was in 2020 in part because the Fed had moved to an "ample reserves" policy implementation framework. The Brookings Institution is financed through the support of a diverse array of foundations, corporations, governments, individuals, as well as an endowment. A list of donors can be found in our annual reports published online here. The findings, interpretations, and conclusions in this report are solely those of its author(s) and are not influenced by any donation. This posting includes an audio/video/photo media file: Download Now |

| You are subscribed to email updates from For LGBTQ+ students, this year’s Pride Month comes at a perilous time. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google, 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

{kind=link}

{kind=link}

{kind=link}

No comments:

Post a Comment