SaaStr |

- 5 Interesting Learnings from Shopify at $4 Billion in ARR

- Salespeople Will Always Exist

- What General Partners at VC Funds Really Do

| 5 Interesting Learnings from Shopify at $4 Billion in ARR Posted: 29 Apr 2021 09:20 AM PDT

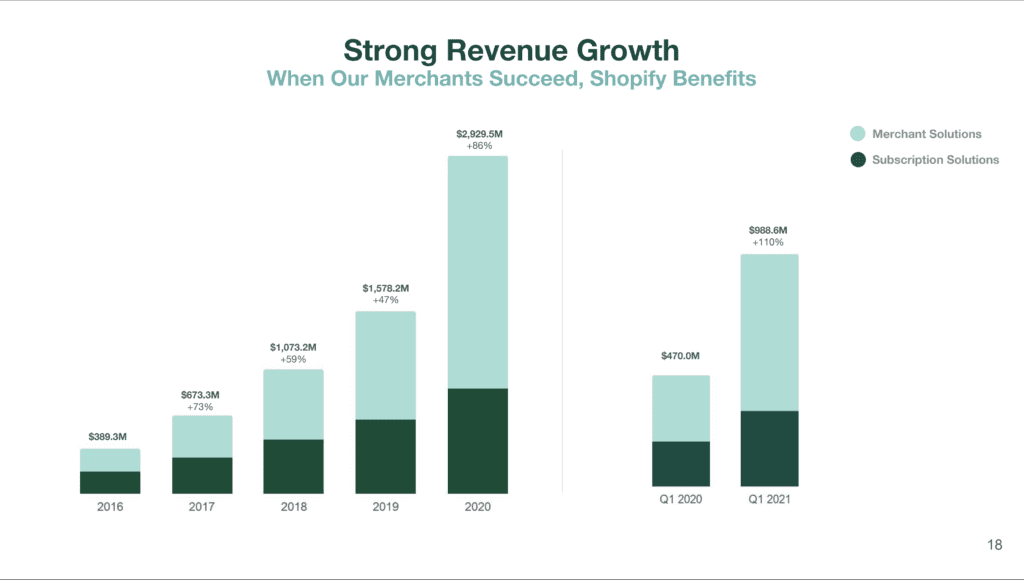

It wasn’t that long ago we checked in at Shopify at $3B in ARR. But Shopify is growing so fast — 110% a year (!) — that we’re already at $4B in ARR. Woah.

Enough has changed that it’s worth doing another deeper dive. 5 Interesting Learnings: #1. The Covid Boost for SaaS. Cloud and ecommerce may end soon, but it hasn’t ended yet. While Shopify projects slowing growth in 2022 post-Covid, it sure hasn’t show up yet. Q1’21 was its fastest growth — ever.

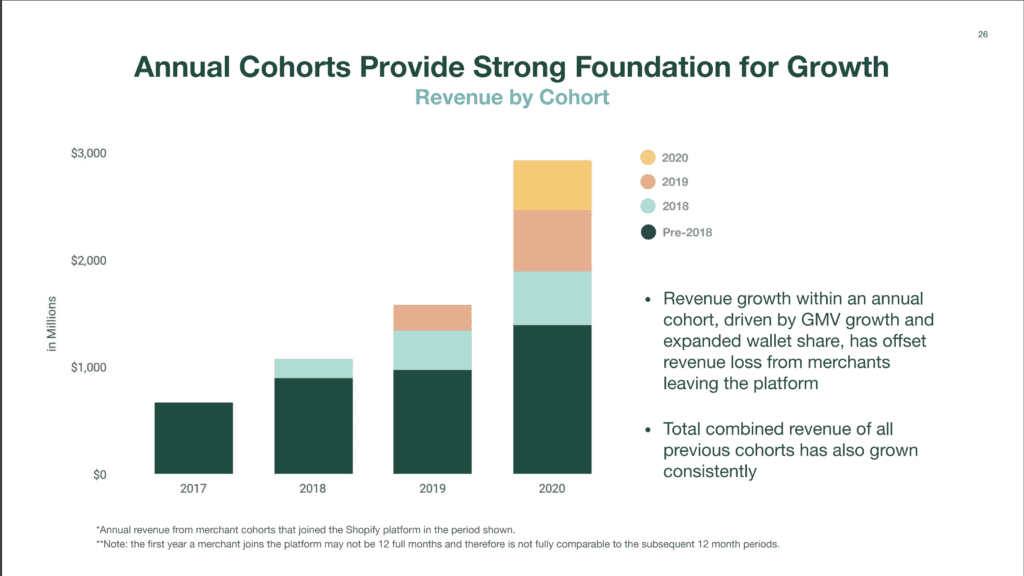

#2. NRR of 110%+ since 2018 — sort of. What is Shopify’s NRR? It would be so helpful to know, as the #1 leader in SMB eCommerce, and also one of the very top leaders in SaaS SMB overall. Well, it’s murky. When you add in payments, i.e. merchant services, NRR for 2018+ is about 110%, based on the below new chart. But likely it’s below 100% excluding payments. After all, many of its customer are single person companies and tiny vendors. If nothing else, it’s a reminder the more value you provide SMBs, the more they pay. By processing payments and more, Shopify has grown its effective NRR from 100% to 110%, and perhaps even more.

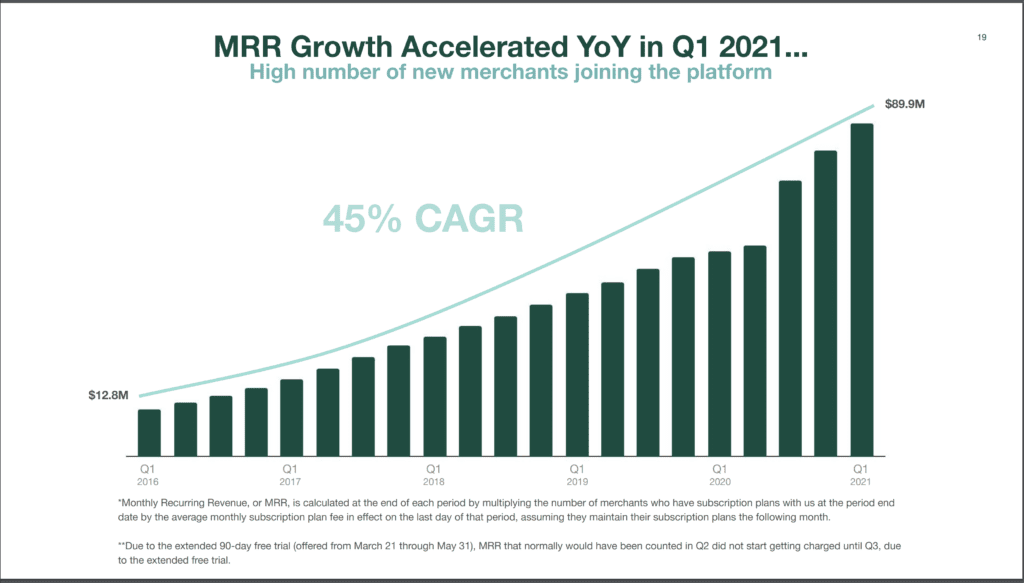

#3. Shopify doesn’t call its non-software revenue “MRR”. A small but interesting note. Most of Shopify’s revenue isn’t SaaS per se anymore, and it only includes actually software revenue in its MRR calculations.

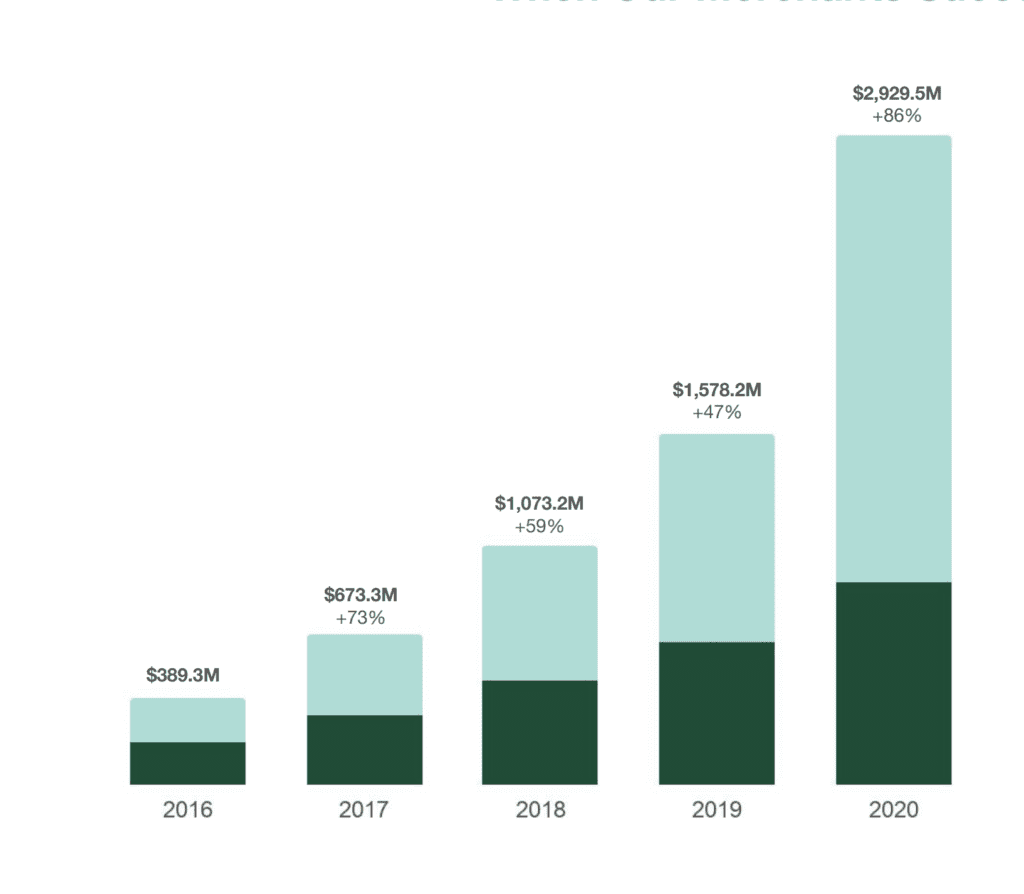

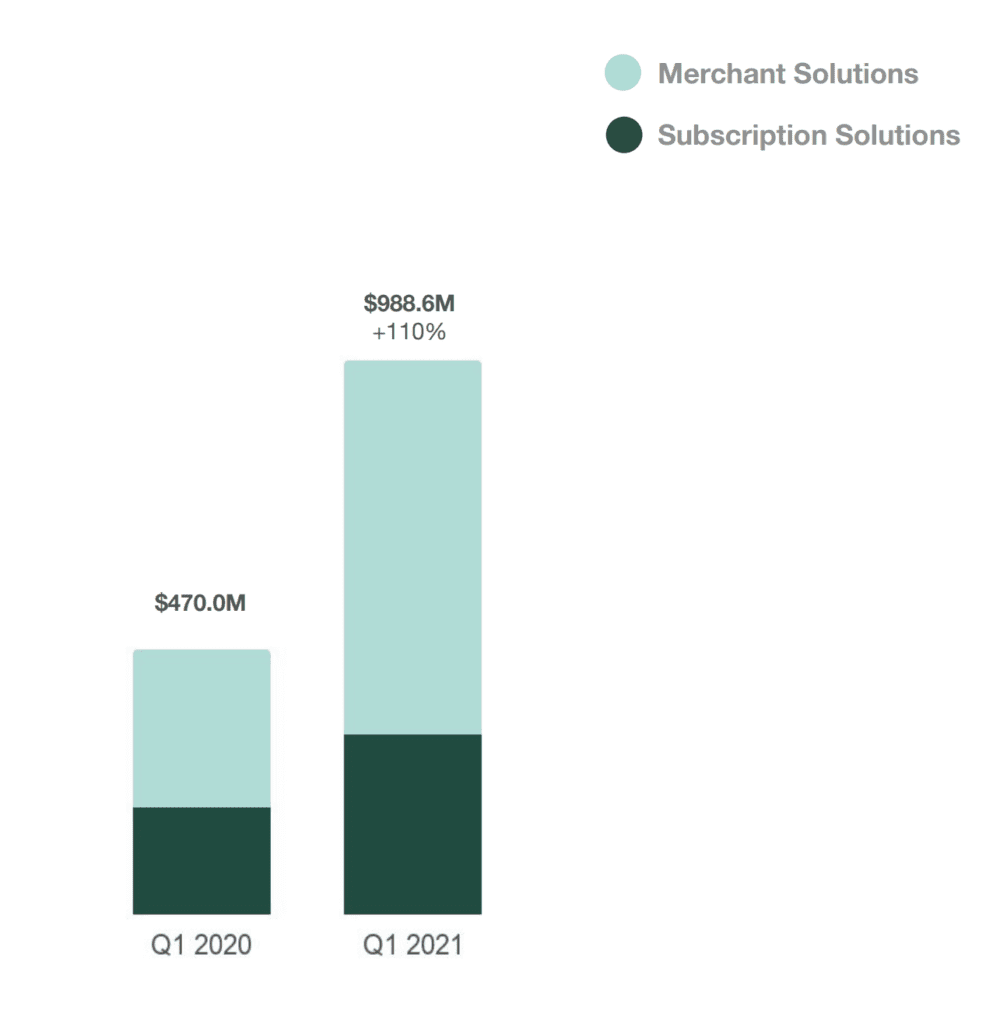

#4. Now clearly a fintech with a layer of software underneath. In 2021 Shopify’s payments and merchant services have pulled even further ahead of its software revenue. We’ve also seen this with Bill.com, where since its IPO, its payments revenue have skyrocketed to 50% of its overall revenues. If you can add a fintech layer to your SaaS product, magic can happen. While SaaS revenue alone grew a stunning 71%, payments / merchant services grew a breathtaking 137% (!).

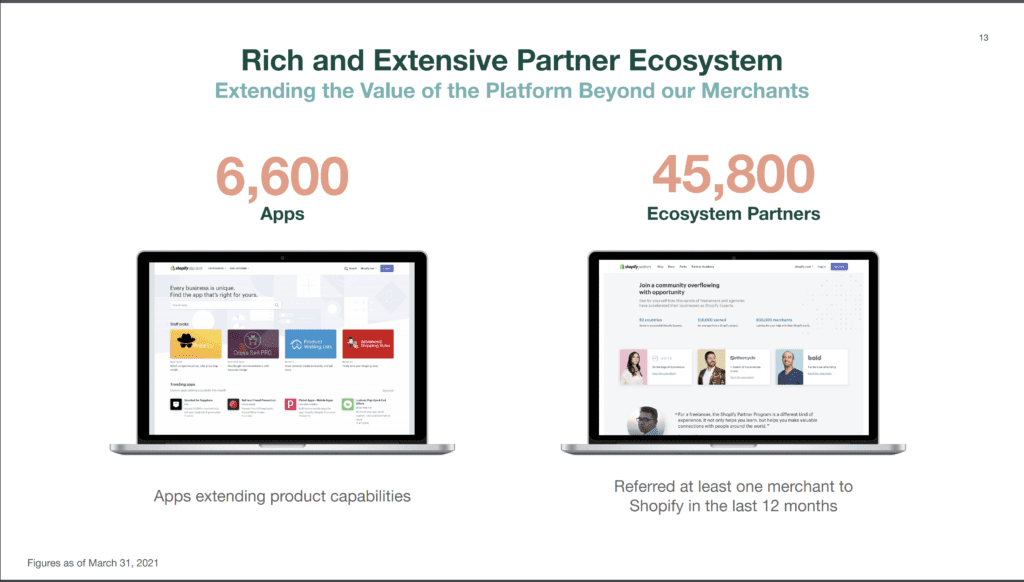

#5. 45,800 partners referred a customer to Shopify in the past 12 months, up 73%. A vivid reminder on how key it is to nurture a partner program, especially if you are a market leader of any sort.

And a few bonus notes: #6. Shopify isn’t getting more enterprise. Its SMBs are growing even faster. We did a deep dive on this here the other day, and it’s super interesting. While Shopify’s enterprise offering, Plus, is doing extremely well, SMBs grew even faster. As a result, Plus (i.e., enterprise and bigger customers) declined from 28% to 26% of Shopify’s revenue. Still a lot. But enterprise isn’t growing faster than SMB as it often does as you scale.

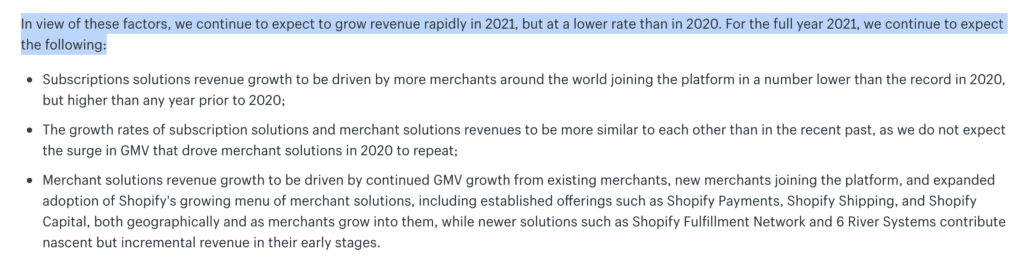

#7. Shopify does expect things to slow down post-Covid. Shopify is still projecting extremely strong growth, but post-Covid, not the record number of merchants joining its platform as they did during Covid.

Wow. 110% growth at $4B in revenues. Not that it’s easy. But don’t let anyone tell you it’s impossible. Really, it wasn’t that long ago Shopify was a $36m ARR start-up. In fact, that’s what it was just back in 2013. The post 5 Interesting Learnings from Shopify at $4 Billion in ARR appeared first on SaaStr. |

| Posted: 29 Apr 2021 05:38 AM PDT Ah, the age-old question of if you really need salespeople these days. Isn’t that kind of … old school? Can’t bots replace them? Well, there are probably at least 3 core true-isms with customer buying:

So for those products: Yes. Done right, salespeople are highly specialized professionals that handle one little piece of the journey — managing and serving the needs of a prospect until it becomes a paying customer. And making sure they take that jump. And yes, there is a bit of friction between those 2 parts of the job.

___________________________________________________________________________ Freemium and self-service are great and you and I love to buy products that way. The other day, I tried to sign up for a $59/month gym membership and a "salesperson" tried to force me to sit down for a 30 minute sales session before I could do my first workout. I walked out. I only had 70 minutes to get in, work out, and get out! A boilerroom process for a $59/gym membership? That makes no sense in 2021+. I just went back to the office and just bought the membership on-line, and walked back. That was faster and easier. Squarespace is IPO’ing at $700m+ without a salesteam, all freemium. Yes, it can work at the bottom of the market, for a tool you can easily use on your own. But prospects for more expensive and more complicated products have questions. Especially, questions about the true risks and true benefits of your solution. And done right, a salesperson is a "free" way to get a resource to answer all your questions. Can you do this without commissions, and without the pressure tactics of a salesperson? Well … maybe. The problem is not only do larger deals require a person to talk to … they also don't close themselves. Often times, they require mapping out business process change. Sometimes, they require discounting and other pseudo-urgency. They require navigating procurement, legal and other stakeholders. You can put a Happiness Officer in charge of all this. But the deals never close at the same rate, at the same velocity, or for the same amount … than if you have a Closing Specialist do the job. So if you want to close deals much more than $299 a month, and you want to close them quickly, for the maximum amount … you'll probably need sales. More here: Curse of the ‘Middlers’: Why Happiness Officers Can’t Stand In for True Sales Professionals | SaaStr and here: Turns out 85% of the World Likes Contact Me. Even Though You Don’t. Can some services scale > $299/month without salespeople? Some, sure. API and B2D products that start cheap can naturally scale higher, e.g. everything from Twilio to Google Adwords and more. Stripe went a long time without a traditional salesforce, as did Slack. Still, they all end up with salespeople. Take a look at this A+ discussion on the topic with Jeff Lawson, CEO of Twilio: You and I don't always want to talk to a salesperson. But seasoned buyers in the F500 don't mind. That's why the skip right to "Contact Me" on your pricing page. They know that a great salesperson is their agent, in many ways. She gets them the data, the information the prospect needs. Sets up the trial. Maps out the business process change. A great salesperson is an enterprise buyer's ally. And those ones — they tend to close a lot of business. (note: an updated SaaStr Classic post) The post Salespeople Will Always Exist appeared first on SaaStr. |

| What General Partners at VC Funds Really Do Posted: 29 Apr 2021 04:48 AM PDT

It can be frustrating in many ways to be part of a large venture firm, be the junior guy that "found"/sourced Facebook-Snapchat-Pinterest-Twilio-Zoom-WhateverUnicorn, convinced the founder to take the money … and then see the General Partner take all the credit. Did they even do anything? Well … yeah. In fact, the managing general partners at a VC fund do a lot more than Zoom-ing into board meetings and meeting with new founders. Remember. VC Firms are investment firms. Money managers. GPs:

The GP-Non GP relationship can be frustrating as the non-GP begins to win and spread her wings. The "part of the management company" vs. "not part of it" relationship can similarly create tensions. But look at the above bullets. The “General Partner” that does all 5 of these bullet points runs the place. No matter how it may look on the website. The post What General Partners at VC Funds Really Do appeared first on SaaStr. |

| You are subscribed to email updates from SaaStr. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google, 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment